Part 5 of a 10 Part Series

TAX BREAKS! Yes, that’s right. There are several ways to reduce your tax bill as a multifamily investor. I will address the five most common today.

1. Depreciation

Most people have heard of depreciation as it relates to their cars. You drive the car off the lot and it immediately loses value. The IRS treats multifamily properties the same way to account for wear and tear. However, there is a HUGE difference with multifamily because the market treats it differently. With the proper maintenance and a strong management team, the property’s value is likely to increase.

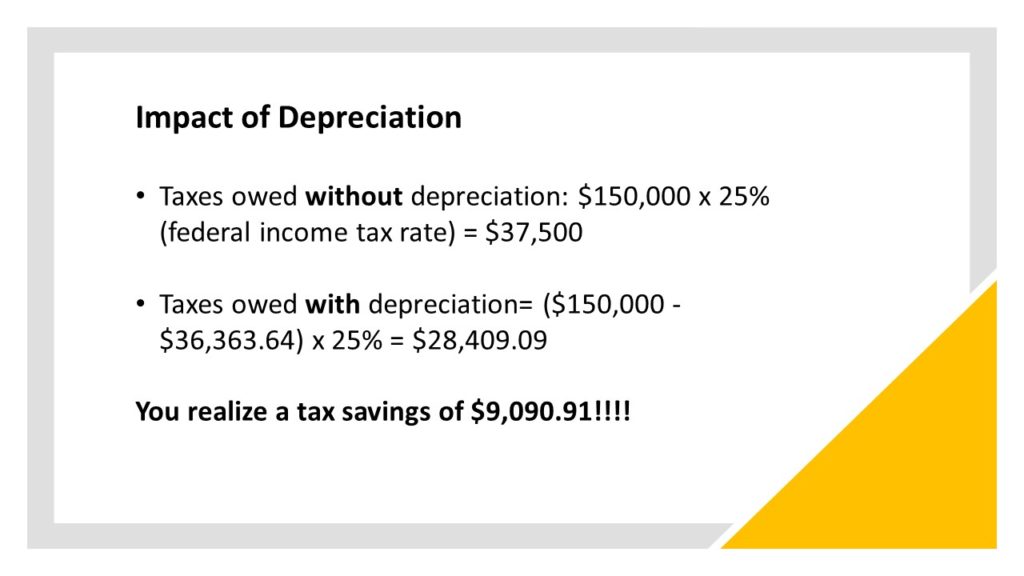

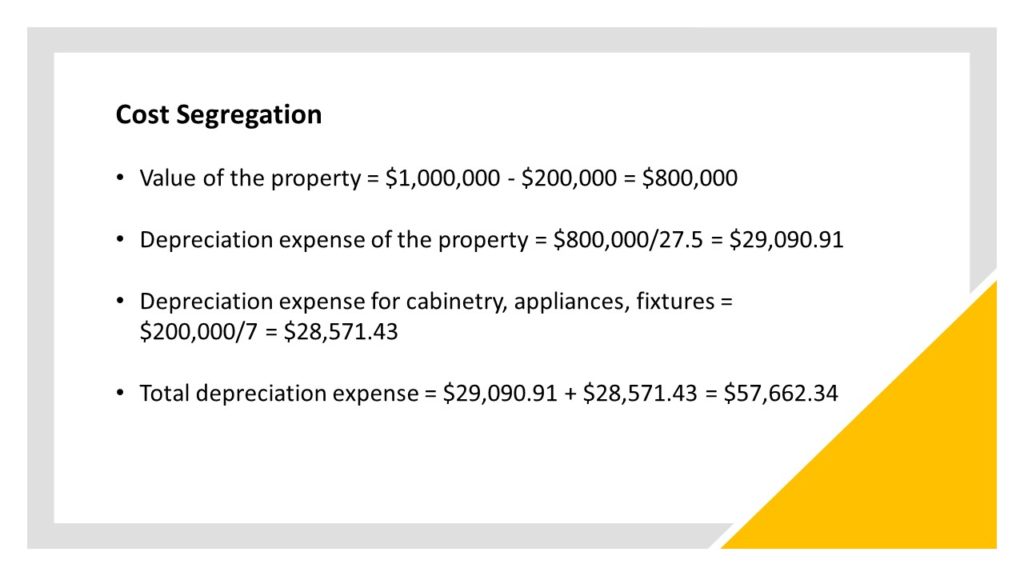

According to the IRS code, multifamily owners are allowed to depreciate their property over 27.5 years. So, to calculate the property’s depreciation amount, all you have to do is to divide the cost to acquire the property by 27.5 years. You will then deduct that same amount each year over the “useful life” of the property.

For example, if you purchase a multifamily property for $1,000,000, your depreciation expense would be $36,363.64 ($1,000,000/27.5). Now let’s assume that the property generates $150,000 per year to demonstrate the impact it would have on your taxes.